Norris Williford, a 22-year-old college senior, doesn’t just work at the MBM Kicks shoe store in downtown Richmond, Virginia — he owns it. And it was a high school class that helped him gain the skills for how to open a business at such a young age.

“Ms. Hayer was actually one of my biggest influences. She taught me a financial literacy class,” Williford said.

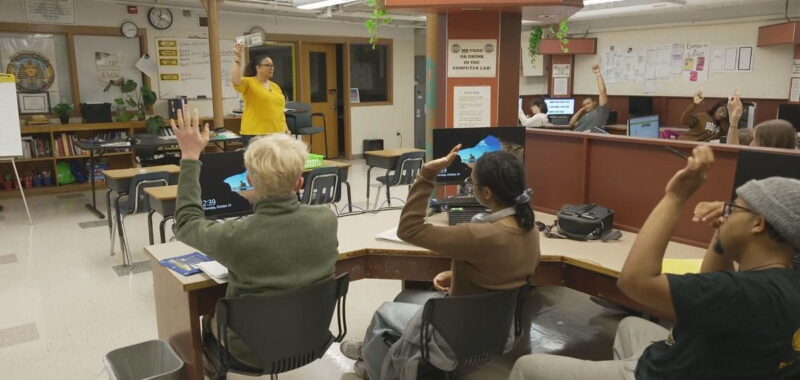

Charlotte Hayer teaches at Richmond Community High School, where a course covering topics like investing, budgeting and saving, is required for graduation.

“I unashamedly tell my students that this is the most important course they will take,” Hayer said.

While 85% of high schoolers nationwide say they want to learn about financial topics, according to business software company Intuit, only 10 states require such a course, according to Champlain College’s Center for Financial Literacy. But by 2031, that’s expected to jump to 26 states.

“They’re entering that phase of life where not a day will go by where they don’t think about money — how to make it, how to save it, how to spend it,” said John Pelletier, the center’s director.

Students who take these classes learn more than just how to budget their money at the mall. Studies show requiring financial education improves credit scores, lowers loan delinquency rates and reduces the likelihood of falling behind on credit card payments.

“If a young person understands how to maximize their credit score, so they get lower interest rates on credit cards, on automobile loans, on their mortgages, that could literally save them more than $100,000 in lifetime interest payments,” Pelletier said.

Mohagany Rogers, a 16-year-old junior, is currently taking Hayer’s class and has started her own business doing other classmates’ hair.

“This class, she kind of teaches us how to get into the mindset of, you don’t always have to buy something that you want. It’s more about what you need,” Rogers said.

It’s a valuable class helping students earn dividends for years to come.